It might not be exactly tropical in your neighborhood yet. But for many of us, it’s finally warm enough to start daydreaming about summer. And that means thinking about getting the yard ready for cookouts, ball games, and gatherings under the stars.

If you’re thinking about the changing seasons, think about making your own fire pit. This popular backyard feature is surprisingly easy to construct, and will bring your outdoor living to the next level. Make a quick trip to the hardware store, grab the kids to help out, and you can have one of these gorgeous backyard features by this weekend!

Are you thinking of adding a fire pit to your yard this year? Is it warm enough in your town yet to even think about spending the evening making s’mores?

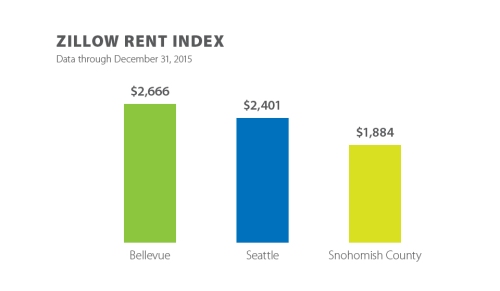

Buying a home in the Puget Sound area beats renting in less than two years, according to anew study. The “breakeven horizon” – the number of years after which buying is more financially advantageous than renting – is 1.9 years.

If you paid the average cost of monthly rent towards a mortgage payment instead, here’s what you could buy:

Based on principal & interest on a 30 year mortgage at 4% interest with 0% down.

Bellevue Monthly mortgage: $2,666 Home value: $558,400

Seattle Monthly mortgage: $2,401 Home value: $502,900

Snohomish County Monthly mortgage: $1,884 Home value: $294,600

Are you ready to invest the money you spend on rent to buy a home?

Get in touch with Oscar and Nancy so we can help you take advantage of the “breakeven horizon” and turn your monthly rent into a mortgage payment!

A severe lack of inventory has led home prices to reach an all-time high. With the supply of properties at its lowest level since 2003, the market is in dire need of more homes to meet buyer demand. That is excellent news for those thinking about selling their home. Sellers can expect a quick sale, favorable terms and a historically high sale price. Buyers will need patience and a strategy for competing with multiple offers.

Eastside

Click image for full report.

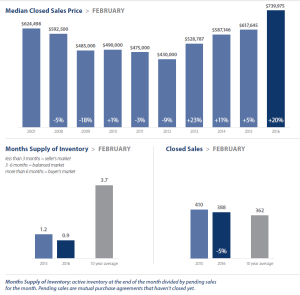

The Eastside, already the most expensive area in King County, saw home prices set a new record in February. The median price soared 20 percent over last year to $739,975. Inventory here is particularly tight, and the area remains a very strong market for sellers. Homes are selling quickly, even at the higher end. A $3.2 million home in Yarrow Point sold last month in just 14 days.

King County

Click image for full report.

The median price of a single-family home sold in February hit an all-time high of $514,975, a whopping 20 percent increase over the same time last year. The number of homes sold exceeded the number that were listed, depleting inventory at a rate that is unsustainable. For the market to remain healthy, more people need to make the decision to list their homes.

Seattle

Click image for full report.

The continued boom in tech company hiring helped propel home prices to peak levels in Seattle. The median price of a single-family home jumped 24 percent over a year ago to $644,950, a new high. Inventory is at critical levels. In the hot Ballard neighborhood there are currently only 17 homes on the market.

Snohomish County

Snohomish County remains a haven of affordability for those sticker-shocked by King County prices. The median price for a single-family home sold in February was $359,000, a moderate increase of 9 percent over the same time last year. However, Snohomish County is struggling with the same historic shortage of homes as King County. With less than a month’s supply, experts expect home prices to continue to increase.

Every three years the Federal Reserve conducts a Survey of Consumer Finances in which they collect data across all economic and social groups. The latest survey, which includes data from 2010-2013, reports that a homeowner’s net worth is 36 times greater than that of a renter ($194,500 vs. $5,400).

In a Forbesarticle the National Association of Realtors’ (NAR)Chief Economist Lawrence Yun predicts that in 2016 the net worth gap will widen even further to 45 times greater.

The Washington State economy has added almost 370,000 jobs since the lowest point of the recession at the start of 2010. Additionally, total employment is 176,000 jobs higher than seen at the 2008 peak. With a vast majority of our metropolitan areas having fully recovered from the job losses seen during the recession, I expect to see somewhat more modest job growth in the coming year. That being said, our economy will continue to expand, which will be a benefit to our region’s housing market.

Home Sales Activity

There were 16,895 home sales during the fourth quarter of 2015, up by 4.6% from the same period in 2014. Sales activity is starting to slow somewhat but this is due to inventory constraints.

The growth in sales was most pronounced in Cowlitz and Lewis Counties and double-digit growth was also seen in Thurston County. Sales declines were seen in Grays Harbor County and Skagit County, but only minimally.

The number of home sales grew in all but two counties, with the average number of sales up by almost 6% from the same period in 2014.

I am not surprised to see some decline in sales start to appear. Listing activity was down by 28% compared to the fourth quarter of 2014, and there were no counties where there were more homes for sale in Q4-2015 versus Q4-2014.

Home Prices

Prices in the region rose by an average of 9.3% on a year-over-year basis but were 0.4% lower than seen in the third quarter of 2015.

Unsurprisingly, no counties saw a drop in average home prices compared to fourth quarter last year.

When compared to the fourth quarter of 2014, San Juan County again saw the fastest price growth with an increase of 37.6%. However, this county is notorious for extreme swings given the huge variations in prices in the San Juan Islands. Double-digit percentage gains were also seen in five other counties.

As long as inventory constraints persist, it is likely that price growth will continue. That said, modest increases in interest rates, in combination with declining affordability conditions in several markets, will likely slow price appreciation.

Days on Market

The average number of days it took to sell a home dropped by nine days when compared to the third quarter of 2014.

It took an average of 78 days to sell a home in the fourth quarter of this year—down from the 91 days it took to sell a home in fourth quarter of last year.

There were just two markets where the length of time it took to sell a home did rise, but the increases were minimal. Jefferson County saw an increase of eight days while Mason County rose by two days. King County remains the only market where it takes less than a month to sell a home.

Conclusions

This speedometer reflects the state of the region’s housing market using housing inventory, price gains, sales velocities, interest rates, and larger economics factors. For the fourth quarter of 2015, I have left the needle at the same position as the previous quarter. In as much as the market is still very heavily in favor of sellers, I fear that some markets are reaching price points that will test affordability. Furthermore, while inventory levels are likely to see some growth in 2016, it will not be enough to satisfy demand, adding further upward pressure to prices. Overall, 2015 was a stellar year with sales volumes and home prices moving higher across the board. In 2016, I believe we’ll see some growth in sales activity, as well as continued price growth – just at more modest levels than last year. Interest rates are going to rise moderately through the year, but still remain very competitive when compared to historic averages. In other words, any increase in interest rates should not be a major obstacle for home buyers. Looking forward, I believe 2016 will be a year of few surprises. Because it is an election year, I do not expect to see any significant governmental moves that would have a major impact on the U.S. economy or the housing market.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.

1. The U.S. will continue to expand with real GDP growth of 2.3% in 2016.

Although a positive number, the forecasted rate of growth suggests that we will be modestly underperforming in 2016. On a positive note, oil prices are likely to remain well below long-term averages, which puts more money into consumers’ pockets in terms of disposable incomes. However, I believe that consumers are likely to continue to save rather than spend which will constrain growth. That said, there is certainly no recession on the horizon – at least not yet – and a strong dollar will act as a bit of an anchor.

2. Employment will continue to expand but the rate of growth will slow. Look for an increase of 1.6% in 2016.

We are rapidly approaching full employment (generally considered to be when the unemployment rate drops below 5 percent). As such, growth in employment has to be driven more by population growth rather than a return to employment. 2015 saw an average of around 210,000 jobs created per month and I believe that this is likely to slow to an average monthly gain of 190,000 new jobs.

3. The U.S. unemployment rate will continue to drop and end 2016 at 4.8%.

As mentioned above, we are heading toward full employment and, as such, the national unemployment rate cannot trend much lower. That said, the less acknowledged U-6 rate (which includes those working part-time and those marginally attached to the workforce) will remain elevated at around 8%, signifying that there is still some slack in the economy and room for the rate to drop a little further.

4. Inflation will remain in check with the Consumer Price Index at 1.9%.

The Federal Reserve has begun the long-awaited tightening of monetary policy and we will likely see the Fed Funds Rate continue to move higher over the next two years. Inflation has yet to respond to the low unemployment rate, but it will.

The core rate of inflation should remain in check and the overall rate could stay below long-term averages as a function of stubbornly low energy costs. Should we see a shift in OPEC’s position relative to oil supply, the overall rate of inflation could rise more rapidly. Oil prices, therefore, will remain in focus during 2016.

The National Housing Market Forecast

5. Mortgage rates will rise, but we will still end 2016 with the average 30-year fixed rate below 5%.

I am taking the Fed at its word when it says that monetary tightening in 2016 will be gradual and heavily data dependent. Accordingly, I expect only a modest uptick in long-term rates in 2016. Furthermore, as long as the Federal Reserve continues to reinvest the dividends that it is receiving from their bond holdings – which is highly likely – the yield on the key 10-year treasury will remain low and hold mortgage rates in check. This is only likely to change after the general election, therefore suggesting that rates will remain very attractive relative to their long-term averages.

6. Credit Quality – which had been remarkably stringent – will relax a little.

Access to credit, specifically mortgage instruments, has not been easy for many would-be homebuyers but that is set to change. I believe that we will see some improvement, specifically for borrowers with “near-prime” credit. This will be of some assistance to first-time buyers; however, credit quality will still be higher than it needs to be.

7. Existing home sales will rise modestly to an annual rate of 5.53 million units with existing home prices up by 4.7%.

I anticipate that we will see some improvement in overall transactional velocities in 2016, but unfortunately, demand will still exceed supply. Prices will continue to rise, but at a more constrained pace than seen over the past few years. This will be a function of modestly rising interest rates as well as slightly improving levels of inventory. I anticipate that we will see more listings come online as more households return to positions of positive equity in their homes.

8. New home sales will jump and be one of the biggest stories for 2016. Look for a 23% increase in sales and prices rising by 3.4%.

I believe that builders will start to build to the entry-level buyer, filling a huge void. Additionally, I see the total number of new home starts increase quite dramatically in 2016 as banks start to ease lending and builders start to believe that the downward trend in homeownership has come to an end. This will help to absorb some of the pent-up demand currently in the market.

9. Foreclosures will continue to trend down to “pre-bubble” averages.

Any story regarding foreclosures will be a non-story as the rate will continue to trend down toward historic averages. However, we will see the occasional uptick as banks work their way through their existing inventory of foreclosed homes. Move along. There’s nothing to see here.

10. The Millennials will start to enter the market.

There are several substantial reasons to expect an increase in Millennial buyers. Firstly, early Millennials are getting older and starting to settle down, and even with modestly higher mortgage rates, rents are likely to continue to trend upward, and this will pull many into homeownership.

Secondly, more favorable mortgage insurance premiums, additional supply from downsizing boomers, and growing confidence in the housing market will lead to palpable growth in demand from this important – and substantial – demographic.

To conclude, it appears to me that 2016 will be a year of few surprises – at least until the general election! Because it is an election year, I do not expect to see any significant governmental moves that would have major impacts on the U.S. economy or the housing market.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.

Along with our partners at the University of Washington, Windermere Real Estate is excited to welcome the Cuban Men’s and Women’s National Rowing Teams as the headlining opponent for the 30th annual Windermere Cup, scheduled for Saturday, May 7, 2016. Rounding out the event will be the Stanford men’s and University of San Diego women’s teams.

The annual spring rowing event on the Montlake Cut is held prior to Seattle Yacht Club’s Opening Day festivities which signal the beginning of boating season in Seattle. The entire event is a joint effort between the University of Washington, the Seattle Yacht Club, and Windermere Real Estate.

Windermere Cup History and 30th Anniversary

The 2016 Windermere Cup matchup with Cuba is significant due to the reestablished diplomatic relations between the U.S. and Cuba on July 20, 2015. It also marks one of the few times a Cuban National Team has competed in the United States since the U.S. and Cuba severed diplomatic relations in January of 1961 during the Cold War, roughly 55 years ago.

The matchup is a fitting tribute to the history of Windermere Cup, which got its start 30 years ago when Windermere Real Estate founder, John Jacobi, joined up with the University of Washington to create the annual rowing event. They wanted to bring the best team in the world to Seattle’s Montlake Cut, which at the time was the Soviets. That occasion marked one of the few athletic competitions for the Soviets inside the U.S. in 25 years, since relations were strained during the 1962 Cuban Missile Crisis. The Soviet Union brought both its men’s and women’s crews and won both races in convincing fashion. After that, the precedent was set for what has become one of the world’s premier rowing events, and certainly a staple of Seattle’s rowing community.

The Windermere Cup will include a number of events during the week leading up to race day. The Seattle Yacht Club’s Opening Day parade through the Montlake Cut will immediately follow the racing.

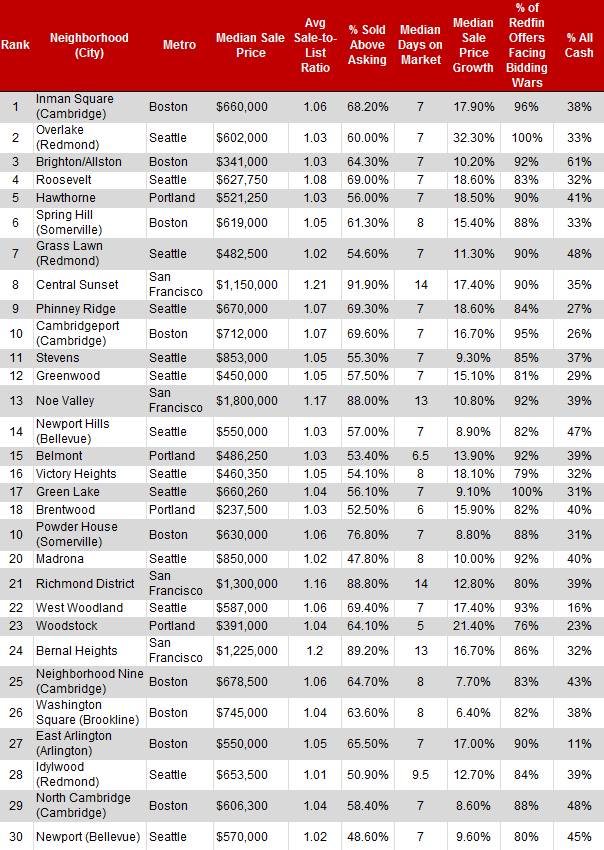

We probably don’t need to tell you that 2015 was a crazy year in real estate, especially in our area. Bidding wars and listings lasting mere days on the market is something we’ve all grown accustomed to. But it turns out we’re not alone. Curbed recently published an article that focused on the 30 most competitive neighborhoods in America. What’s the most mind blowing thing about this list? Of the 30 neighborhoods listed, 13 of them are in King County.

The Eastside was well represented on this list with Bellevue and Redmond making huge claims. Overlake was was the second-most competitive market in the entire nation! Honorable mentions were Grass Lawn (#7), Newport Hills (#14), Idylwood (#28), and Newport (#30).

It’s hard to say exactly what 2016 has in store, but our very own Chief Economist, Matthew Gardner, has a few ideas (such as expecting that housing in Seattle will continue to appreciate in value, but at a slightly lower rate than 2015).

We're nearing the end of the year and everyone is sharing their predictions and hopes for real estate in 2016. According to Realtor.com, here are the top five trends that will be shaping real estate next year. The economy, rental market, and housing market are all changing in the Seattle area and its Eastside. These trends are definitely something you want to pay attention to as we jump into 2016.

Five Real Estate Trends in Real Estate in 2016

1. We'll Return to Normal

Something that we in the Seattle area are eagerly anticipating! The year ahead will see healthy growth in home sales and prices, but at a slower pace than in 2015 according to Realtor.com. "Distress sales will no longer be playing an outsized role, new construction is returning to more traditional levels, and prices rise at more normal rates consistent with a more balanced market."

2. The Best Year to Sell

We all knew that millennials would make a huge impact in 2015, and they did. Millennials emerged as a dominant force in 2015 and represented almost 2 million sales. That's more than one-third of the total! "This pattern will continue in 2016 as their large numbers combined with improving financial conditions will enable" them to jump into the market again. Financially recovering Gen Xers and older boomers who are thinking about retirement are also going to affect the market. According to the article, since "most of these people are already homeowners, they'll play a double role, boosting the market as both sellers and buyers."

For more information, read the full list on Realtor.com.

After seven years of some of the lowest interest rates in recorded history, the Federal Reserve has decided to raise the key Fed Funds Rate by 0.25 percent, which is causing some to be concerned that it will lead to a jump in mortgage rates and negatively impact the US housing market.

So, the question everyone wants to know is, do we need to worry about interest rates leaping?

While I expect there to be some volatility in rates for a while, I don’t believe the real estate market will implode in a rapidly rising interest rate environment. So, yes, interest rates are going to rise modestly, but no, I don’t think we need to be overly worried about it.

To qualify this statement, we need to understand that mortgage rates do not run in “lock-step” with the Fed Funds Rate. Although the Fed Funds Rate is a bellwether for the greater economic environment, there have been times when these two rates have moved in opposite directions, such as we saw in 2004/2005.

It’s also important to understand that while interest rates for revolving credit, such as credit cards and home equity loans, are tied to the Fed Funds Rate, non-revolving loans – like mortgages – are not. Mortgage rates are tied to bond yields – specifically the 10-year treasury.

So what do I think will happen?

I believe interest rates will rise above 4 percent, but we will not see a sharp spike in rates. The Fed has stated that any upward movement in the Fed Funds Rate will be slow and steady, and will reflect the greater economy. And I believe that mortgage rates will follow suit. Additionally, mortgage rates have already moved higher in anticipation of an increase in the Fed Funds Rate.

That said, it is worth noting that any weakness in the global economy can actually have a downward effect on interest rates. This is referred to a “flight to quality”. In essence, investors seek safe haven during times of economic uncertainty. If markets outside the U.S. continue to underperform, there will likely be increasing demand for bonds which will drive up their price and drive down interest rates. Between China, the Eurozone, war in the Middle East, and a massive drop in oil prices, it's certainly possible that the price of mortgage backed securities could rise, leading U.S. mortgage rates lower.

Interest rates could not realistically stay at their current levels forever. But an increase should not be a great cause for concern. Yes, an increase makes mortgages more expensive, but not to a point where they will have a negative effect on home values. That said, the rate of home price growth will undoubtedly slow in the coming year, but that isn’t necessarily a bad thing.

A little perspective might help: the average rate for a 30-year loan in the 1970’s was nine percent. It was 13 percent in the 1980’s and eight percent in the 1990’s. And yet people still managed to buy and sell homes throughout those years. With that in mind, the rate increases we’re likely to see in 2016 are nothing to fret over.

The increase in the Fed Funds Rate should be taken as a sign that our economy is expanding and is a preemptive move to limit anticipated inflation. While interest rates have risen from their all-time low, they are still remarkably favorable. And will remain so through 2016.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

This speedometer reflects the state of the region’s housing market using housing inventory, price gains, sales velocities, interest rates, and larger economics factors. For the fourth quarter of 2015, I have left the needle at the same position as the previous quarter. In as much as the market is still very heavily in favor of sellers, I fear that some markets are reaching price points that will test affordability. Furthermore, while inventory levels are likely to see some growth in 2016, it will not be enough to satisfy demand, adding further upward pressure to prices. Overall, 2015 was a stellar year with sales volumes and home prices moving higher across the board. In 2016, I believe we’ll see some growth in sales activity, as well as continued price growth – just at more modest levels than last year. Interest rates are going to rise moderately through the year, but still remain very competitive when compared to historic averages. In other words, any increase in interest rates should not be a major obstacle for home buyers. Looking forward, I believe 2016 will be a year of few surprises. Because it is an election year, I do not expect to see any significant governmental moves that would have a major impact on the U.S. economy or the housing market.

This speedometer reflects the state of the region’s housing market using housing inventory, price gains, sales velocities, interest rates, and larger economics factors. For the fourth quarter of 2015, I have left the needle at the same position as the previous quarter. In as much as the market is still very heavily in favor of sellers, I fear that some markets are reaching price points that will test affordability. Furthermore, while inventory levels are likely to see some growth in 2016, it will not be enough to satisfy demand, adding further upward pressure to prices. Overall, 2015 was a stellar year with sales volumes and home prices moving higher across the board. In 2016, I believe we’ll see some growth in sales activity, as well as continued price growth – just at more modest levels than last year. Interest rates are going to rise moderately through the year, but still remain very competitive when compared to historic averages. In other words, any increase in interest rates should not be a major obstacle for home buyers. Looking forward, I believe 2016 will be a year of few surprises. Because it is an election year, I do not expect to see any significant governmental moves that would have a major impact on the U.S. economy or the housing market.

Along with our partners at the University of Washington, Windermere Real Estate is excited to welcome the Cuban Men’s and Women’s National Rowing Teams as the headlining opponent for the 30th annual Windermere Cup, scheduled for Saturday, May 7, 2016. Rounding out the event will be the Stanford men’s and University of San Diego women’s teams.

Along with our partners at the University of Washington, Windermere Real Estate is excited to welcome the Cuban Men’s and Women’s National Rowing Teams as the headlining opponent for the 30th annual Windermere Cup, scheduled for Saturday, May 7, 2016. Rounding out the event will be the Stanford men’s and University of San Diego women’s teams. and won both races in convincing fashion. After that, the precedent was set for what has become one of the world’s premier rowing events, and certainly a staple of Seattle’s rowing community.

and won both races in convincing fashion. After that, the precedent was set for what has become one of the world’s premier rowing events, and certainly a staple of Seattle’s rowing community.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.